Although Hawaiian Electric has been much in the news since the fire that destroyed Lahaina last August, here’s something that hasn’t been talked about much.

There’s a class of victims in the Lahaina fire disaster that hasn’t been mentioned publicly yet, at least that I’ve been able to find.

I’m talking about the thousands of Hawaii retirees who lost up to 3/4 of their retirement savings when the value of their investments in Hawaiian Electric Industries, the parent company of Hawaiian Electric Company, or HECO, plummeted almost overnight in the days after the fire.

While institutional investors with their computerized trading systems and full-time investment managers got out from under the HE stock without major damage, most retirees are “buy & hold” investors who just aren’t that nimble when things go topsy-turvey.

One recent estimate is that individual retail investors hold 35.59% of the company stock.

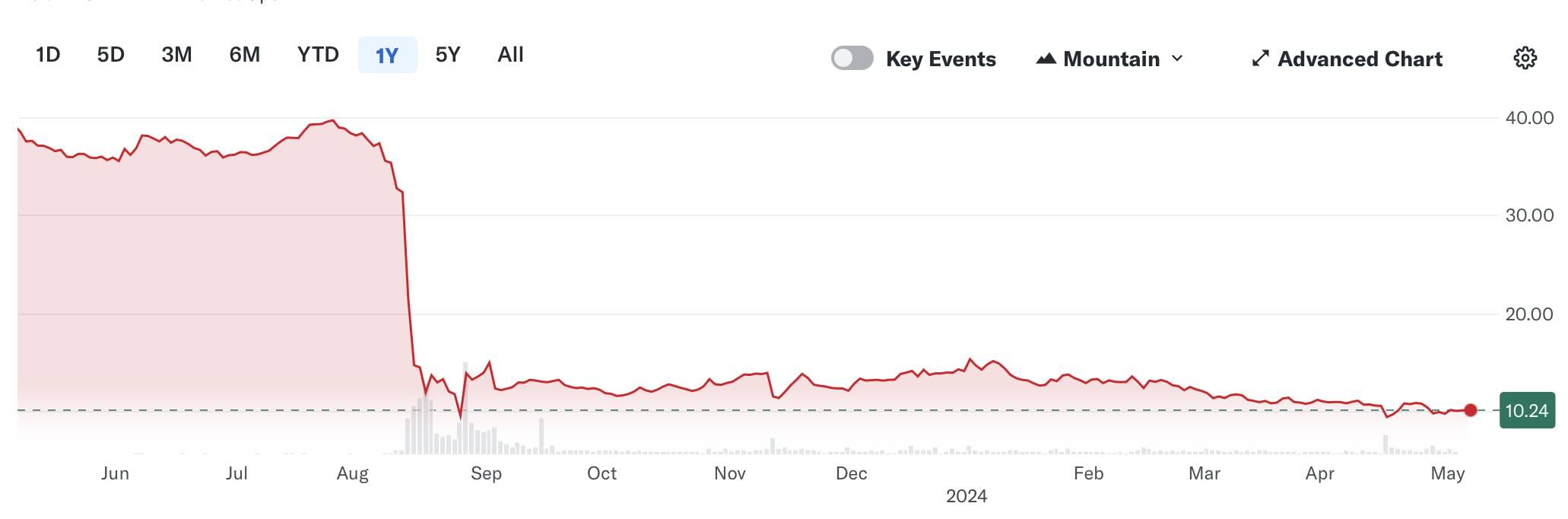

One financial website reported: “The share price as of May 17, 2024 is 11.50 / share. Previously, on May 22, 2023, the share price was 36.29 / share. This represents a decline of 68.31% over that period.”

Yes, sadly, I’m part of that group. I inherited a nice retirement nest egg from my mother, who had invested small amounts in Hawaiian Electric many decades ago, and followed the conservative path by just reinvesting the dividents, letting the number of shares, and the overall value, continue to slowly grow.

Over at least 60 years, that’s a lot of compound growth. And I had continued in the same vein. After all, what’s more stable, in the long run, that a local utility subject to state regulation, including a guaranteed rate of return on the company’s investments in infrastructure? It wasn’t a growth stock, but it appeared to be one that allowed the retirees who owned its stock to sleep at night.

I attended several annual stockholder meetings while the NextEra buyout was being debated. There were a whole lot of middle class folks who were there because their retirement incomes were at stake. I wish that I could provide numbers of individual stockholders here in Hawaii, or who formerly lived here but have since moved elsewhere. But the meetings were held in very large ballrooms, and those present likely represented an even larger group that didn’t attend.

They were doing fine.

Until the fire. Then they all took a double hit. First, the stock’s value plummeted, as did the value of their retirement assets. And HEI stopped paying a dividend, meaning that those who were relying on those dividends to supplement their social security and pensions were suddenly facing harder times.

It’s fair to say that these shareholders are better off than those who lost their lives or their property in the Lahaina fire. But some, I’m sure, many who assumed they were comfortable are facing new and worsening financial hardships as the company’s prospects are difficult at best.

Here’s a chart of Hawaiian Electric Industries stock price in the months before and after the fire from Yahoo Finance. Imagine your savings taking that sort of hit.

Discover more from i L i n d

Subscribe to get the latest posts sent to your email.

WOW, this is extremely important, Ian. Thanks for the heads up!

Good point Ian. I too invested in HE and sold at the time of Next Era. What was unusual, and made it an attractive “widows and orphins” stock was the high dividend that was always paid, $1.20 per share, annually. Paid in quarterly increments, so it compounded quarterly. The other side of that rather than use a substantial portion of its profits to reinvest in the utility infrastructure it went to dividends. So for example the oil fired generators now used have to operate at some high level, burning fuel, no matter what the demand. Simply investing in demand adjustable generators would have reduced costs, and global warming emmissions by 25 percent. The second point is it made high electrical bills acceptable. Like 2 to 3 times higher per kilowatt hour. That is THE high business cost here that distorts our economy. Now there is an effort to set up a second larger film studio, with government support, and films consume a lot of electricity. So one of the basic costs will be up to 3 times higher than elsewhere. And solar and wind prices are pegged to those generators. So wind power, that costs 6 cents per kwh to produce is bought for 18 cents by HE, and rate payers buy that from HECO. And the legislature has enshrined this by telling the PUC to ignore pricing in order to foster renewable energy.

I’ve been watching this stock for many months, even before the fire looking for a buy in point, all for the same reasons you mention. Glad I’ve held back. I still haven’t bought in even at this bargain price because of the wildcard of potential bankruptcy. I wish all you Hawaiian Electric Industries stock holders the best and look forward to being one among you, but not yet.

Would a HECO bankruptcy have any effect on HECO retirees?

Here’s a link to the company’s latest annual report. There must be relevant information buried somewhere in it.

https://d18rn0p25nwr6d.cloudfront.net/CIK-0000354707/c97d248d-eb7d-428a-a96a-f5a03eabe6c1.pdf

My question relates to the assets of HECO’s retirement system, not the loss in value of HECO stock.

I think you might find useful information in HECO’s pension fund report to its members. Don’t know if it’s a public document but if you know an employee/member, maybe they would share.

Great good always follows tragic events. I pray for those who have lost the most.

But I just read that at the stock holders meeting that was just held, 70+% voted to approve the ridiculously high salaries last year of the executives! Doesn’t sound like many people are really worried about their own retirement.

Please define “ridiculously high”. Salary is not based on worth, but replacement cost. For example, fast food is built on being able to use anyone. But an experienced high-level admin with a track record in a large industry isn’t that common. There’s competition for them. If you’re not paying the going rate, then you’re going to have a vacancy. I’d also suggest doing the math. A quick calculation suggests the CEO salary amounts to half a penny per stock.

If HECO was paying $1.20 per share annually with the stock price at $35 a share that’s only 3.4% – not exactly a princely reward. In the US privately owned utilities are really creatures of the state. They are so heavily regulated that everything they do or don’t do is really almost at the direction of the state public service commission which sets the rules and allows them to make a modest profit.

At Berkshire Hathaway’s annual meeting this year they werre talking about how the western US power companies had been beaten up by wildfires and that if the states want power companies to invest in plant and equipment the states have to set rules which allow them to make a profit.

This is spot-on and describes exactly the situation for many local HEI investors. We never took dividends in cash either and instead rolled them over into additional stock. Over the years, it added up.

I don’t understand if you are actively in retirement why you would have the majority of your “nest egg” in a single utility stock? This is why you diversify, or better yet invest in something like VTSAX? Why risk it all on a single company vs. investing in a slice of 100’s of American companies? Personally, this sounds like extremely poor retirement plan…Pick a mutual or index fund with the lowest fee possible (ahem Vanguard).

Also, even if you invest in a mutual fund/index fund, you must be prepared to hold out through the inevitable market crashes. Overall, the market historically has always gone up, but you must have a plan in place to survive the lows, when it is no longer feasible to “pull the 4%”.

I agree with most of your points. And don’t worry, we didn’t “risk it all” on Hawaiian Electric. But it still stings.