In late 1942, my dad signed a contract and paid a $100 downpayment to purchase a new 3-bedroom house on a lot in Kahala. The back yard flowed over into one of the famrs that filled most of the interior of Kahala at that time. Among those living along Kealaolu Avenue were war workers and hookers. The offer to pay $6,000 for the small 3-bedroom house on a 11,250 square foot leasehold lot was accepted. By the time the deal closed, $100 had been knocked off the price because of what my dad said was a scratch on the floor.

Here’s a copy of the original real estate contract.

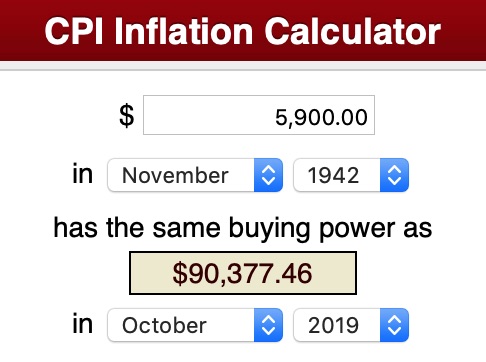

When I ran into this receipt, I wondered what that $5,900 would be worth in today’s dollars. I turned to the Consumer Price Index Calculator available from the Bureau of Labor Statistics.

It came up with the answer: It would be equal to $90,377.46 in today’s dollars.

Is there anything remotely comparable that you could buy today for $90,000? Short answer–No. Nothing close.

To be fair, the area wasn’t considered that desirable in 1942. It was just a normal neighborhood backed up to neighboring farms. But it had bus service, was relatively close to shopping, and close to the beach. And by today’s standards, it’s considered a large lot.

How did it that 1942 price tag compare to the cost of the first apartment we bought back in 1978?

The original $5,900 would have been worth about $22,651.79 in 1978, according to the CPI calculator. We had to pay 2-1/2 times that for a 2-bedroom townhouse near Kahala Mall. So housing had gotten more expensive, but was not totally out of reach.

Today is another story. You can still buy raw land in the boondocks for under $90,000 but not with a house, unless it’s on leasehold land with exorbitant lease rent.

It’s just a small example of how fast we’re moving away from the concept of affordability.